by Ben Jennings, Lead Advisor, CFP

Over the next few weeks, our perspective may become a bit more international as we focus on football in Seattle. No, not the Seahawks, silly - the World Cup.

As we try to find timely hooks that will entice you to read our newsletter, this seems like an apt moment to share an article with an international flair. So here goes.

Last year, I could have gone to my high school class's 50-year reunion, which means I am starting to think I may be able to claim a perspective based on long-term experience. Let's look together at a few aspects of investing over the past 50 years.

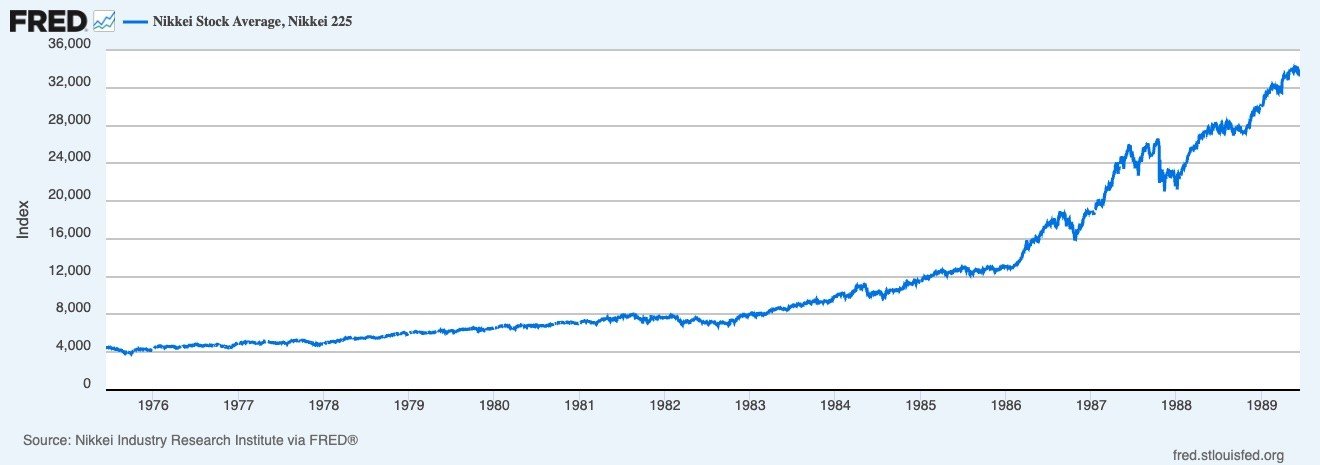

I was curious and used data from the Federal Reserve Bank of St. Louis to look back over that period. If I had looked at the history from when I graduated high school in 1975 to business school in 1989 - yes, I managed to cram four years of college into 14 years - investing in the broad Japanese stock index, the Nikkei, would have seemed like a sound idea at the time.

Nikkei 225 chart rising from 1975 to 1989.

Nikkei 225 chart declining from 1989 to 2003.

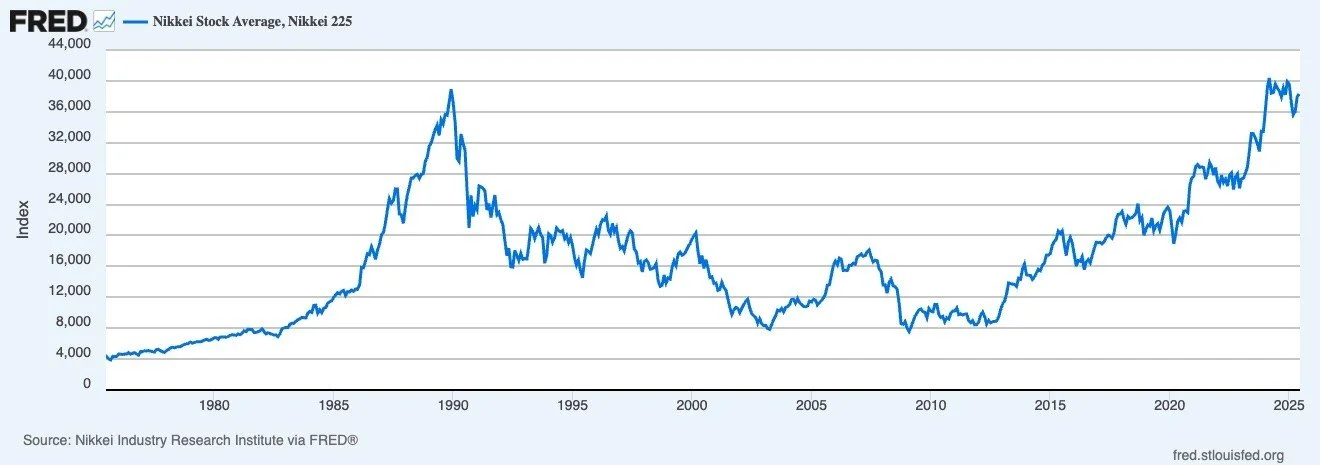

So, what would the next 14 years of that investment have looked like?

Not as good as I might have hoped. Truth be told, after celebrating my college graduation along with the Japanese market celebrating its all-time high, both of us would have some challenging times ahead.

Indeed, though 14 years might seem like a long-term investment horizon, my investment in the Japanese stock market would actually have needed another two decades to recover.

Nikkei 225, 1975-2025. Japanese stocks did not regain their 1989 high until 2023. Source: Nikkei Industry Research Institute via FRED.

Yes, following that 1989 peak, Japanese stocks needed until 2023 - 34 years - to get back to their previous high. But if I had somehow had the endurance to hang on to the investment over the entire 50 years after high school, I would at least have earned an annualized return of 4.6%.

I know. Less than impressive, right?

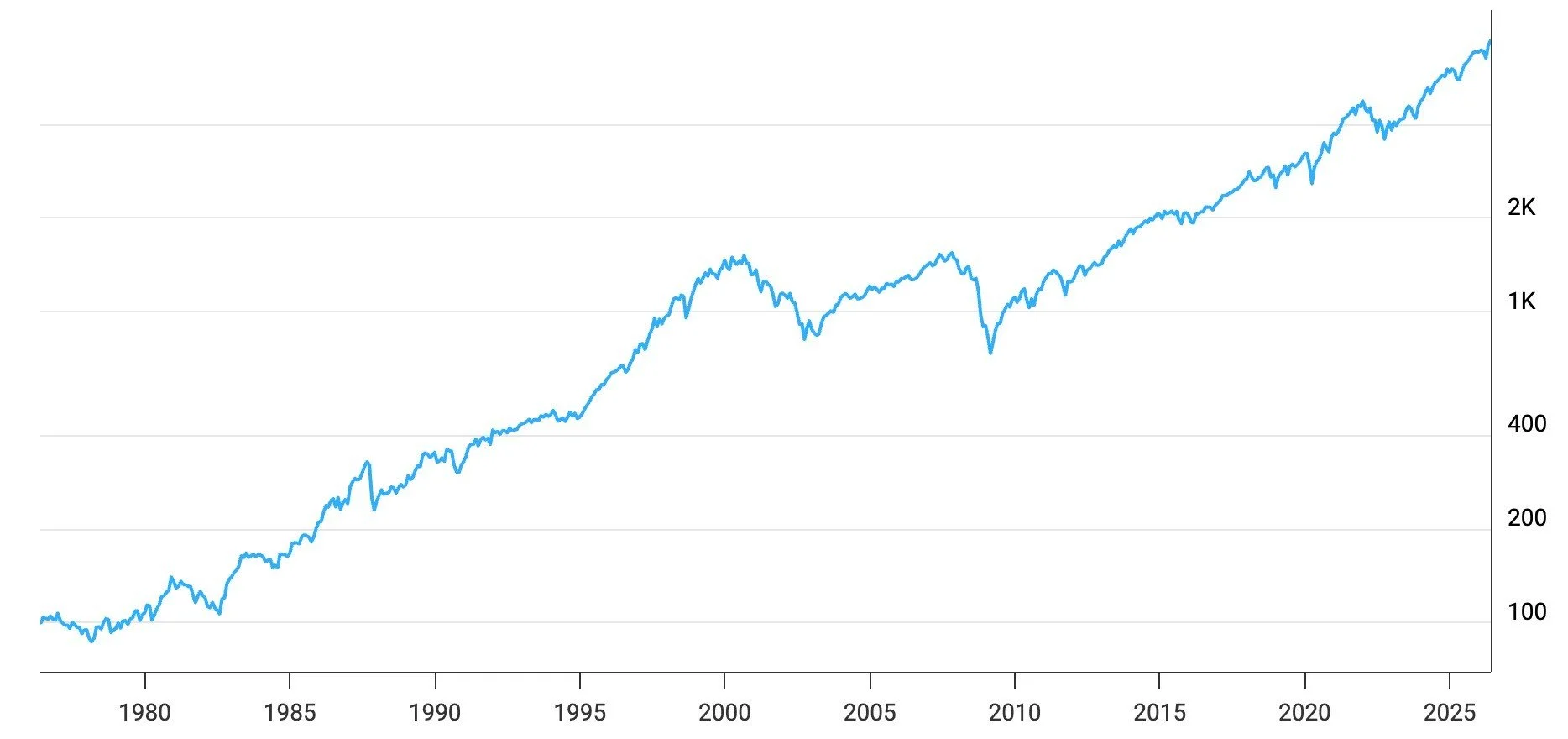

My Japanese stock investment over the long run would have looked even less impressive if you knew what large-cap U.S. stocks returned over that same 50-year period.

Large-cap U.S. stocks returned about 8.6% annually over the same 50-year period.

So this article is supposed to be about why we invest internationally, right? How am I doing so far?

The truth is that the recent past has been a relatively disappointing time to diversify internationally if your goal is to earn better returns. And while those of you who have already had annual reviews probably had your advisor point out the finally strong returns from non-U.S. stocks last year - close to 28% versus about 16% for U.S. stocks in 2025 - the comparison for 2026 depends on when we had your meeting.

As of this writing, May 26, 2026, large U.S. stocks lead non-U.S. stocks for the year-to-date, 1-year, and 3-year periods. So, recently, international investing has not done much to increase returns.

Diversification Is About Risk, Not Just Return

However, the goal of diversification - and international stock diversification specifically - is not necessarily to increase returns. It is to dampen risk.

Financial author and Northwest native William Bernstein has noted that risk, or volatility, can be thought of in two dimensions:

Depth: The size of the loss.

Duration: The time it takes to recover from the loss.

Based on these dimensions, Bernstein describes two types of risk.

The first he calls shallow risk: "a loss of real capital that recovers relatively quickly, say within several years." This is the kind of risk we at SoundView hope to manage primarily through perspective and discipline. We remind clients that, across long-term history, stocks have negative returns about once every three to four years, and we encourage you to keep perspective and ride things out. The key tool here is discipline.

The other type of risk Bernstein calls deep risk: a loss of real capital with a duration so long that few investors will persevere through it, often resulting in a permanent loss of capital.

In my experience, declines in value that persist for more than 10 years, like the Japanese stock market example beginning in 1990, are tough for investors to stay the course through. It turns out our primary tool here is not discipline, but diversification.

International Stocks And Deep Risk

So, how have international stocks helped with deep risk, meaning declines over a long duration that many investors probably would not ride out?

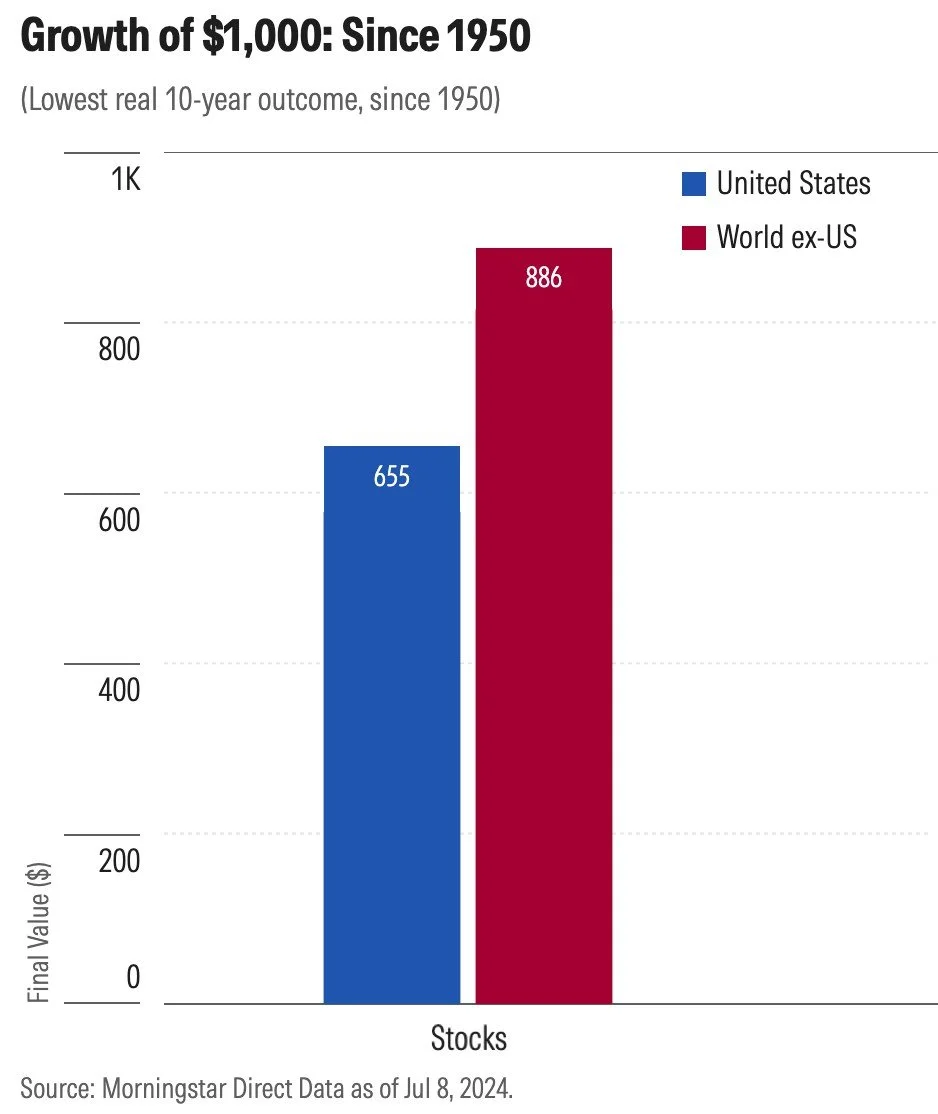

Growth of $1,000 during each market's lowest real 10-year outcome since 1950.

Here is a chart from Morningstar that recaps the worst 10-year period since 1950 for two broad stock markets: the United States and the rest of the world.

$655 Final value for $1,000 in the worst 10-year period for U.S. stocks.

$886 Final value for $1,000 in the worst 10-year period for non-U.S. stocks.

It turns out that the worst 10-year periods for international stocks since 1950 have been far less severe than the worst 10-year periods for U.S. stocks. During the worst 10 years for U.S. equities, $1,000 shrank to $655, a loss of 34.5%. By comparison, during the worst 10-year stretch for international equities, $1,000 declined to $886, a loss of only 11.4%.

So, while international investing has been a drag on portfolio returns of late, history shows us that we can expect non-U.S. stocks to earn their keep in a portfolio by reducing exposure to deep risk.

The typical SoundView investor is not trying to get rich by chasing the highest possible return. Most are trying to avoid being poor by managing risk thoughtfully. From that perspective, we believe we are serving you well by including international stocks in your portfolio.

So until we can get back to Seahawks football, find an opportunity to enjoy some of the World Cup and reflect on the joys of being international.